How to generate value with data monetization in banking

What if the most valuable product your bank could offer isn't a new loan, app, or card but the data it already holds? Monetization of data in banking is about turning existing information, such as tra...

What if the most valuable product your bank could offer isn't a new loan, app, or card but the data it already holds?

Monetization of data in banking is about turning existing information, such as transactions, risk profiles, and customer behavior, into something that creates measurable value. That might mean generating revenue through secure APIs for partners, improving credit scoring with alternative data, or reducing fraud losses using patterns your systems already track. It's not about selling sensitive or personal data. It's about structuring, securing, and aligning it with clear business outcomes.

If your bank has data assets but lacks a plan to generate returns from them, this guide will help you examine what data monetization in banking is, its use cases, and what gets in the way of making it work.

What value does data monetization bring to banking?

Whether through internal efficiencies, external data products, or embedded financial services, banks are beginning to realize that their data is one of their most valuable commercial assets. To put it into perspective, here's what becomes possible when data is treated as a monetizable resource:

- What if you could turn underutilized customer data into a revenue-generating product? Data monetization enables banks to sell anonymized insights, license APIs, or provide benchmarking services.

- What if customer profiles were no longer static, but evolved with every transaction? Banks can dynamically personalize offers, credit options, and financial advice, driving stronger engagement and higher customer lifetime value.

- What if fraud prevention tools became revenue streams? By externalizing fraud analytics, such as real-time anomaly detection or merchant-level risk scores, banks can create licensed fraud-as-a-service offerings for partners and platforms.

- What if lending decisions weren't based on incomplete credit reports? Integrating behavioral data, open banking insights, and transaction metadata improves affordability models and reduces default risk, especially in underserved segments.

- What if clients started paying for the market intelligence you already hold? Retailers, insurers, and investors are willing to pay for access to consumer spending patterns, geographic trends, and competitive benchmarks derived from your transaction data.

- What if data became the foundation for new business models? Data monetization in banking enables to expand into para-banking, offering advisory services, insurance, or investment products based on a granular understanding of each customer's journey.

As the strategic potential becomes clear, the next question is how to transform it. Below are five proven of data monetization banking use cases, each tied to real business problems and outcomes.

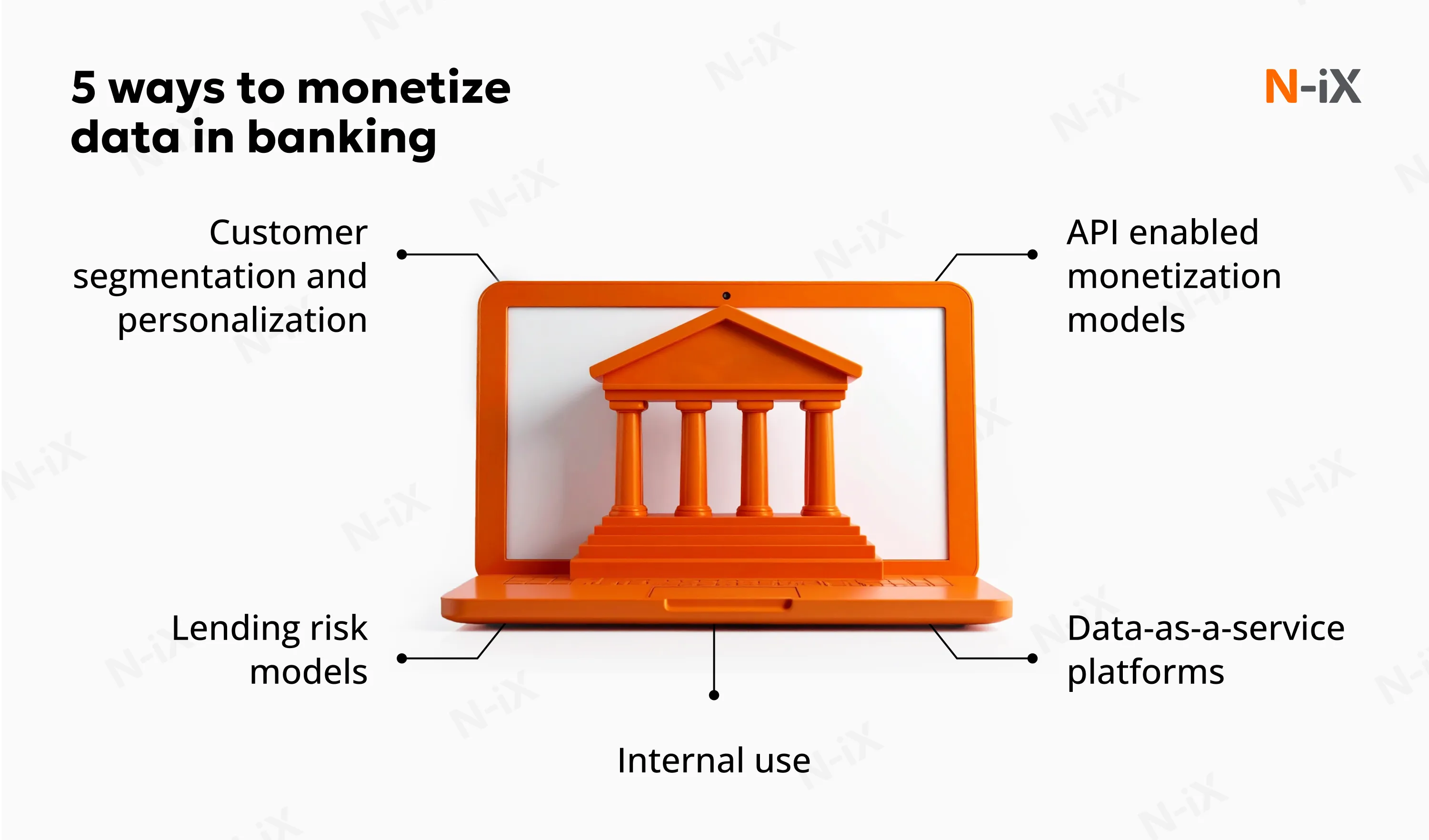

5 ways to monetize data in banking

1. Customer segmentation and personalization

What if banks could predict customer needs before they're even expressed? Data-rich banks can transform segmentation from static demographic profiling into a real-time, high-resolution understanding of customer behavior. Banks identify microsegments with precision down to behavioral triggers and product affinities using unsupervised learning techniques (e.g., K-means clustering, DBSCAN), combined with life-stage event data and transaction flows. Such an approach enables dynamic personalization across channels tailored to adaptive pricing, content, and feature sets.

Take the example of how large retail banks merge purchase categories, geolocation, and interaction frequency to generate segment-specific loyalty campaigns. Instead of broad tiers, customers are grouped by behavioral clusters, e.g., frequent travelers who prefer mobile banking and show strong debit usage in airport locations. These segments receive geo-triggered offers from partner merchants or dynamic point conversion for cross-brand benefits.

Beyond marketing, segmentation informs the design of new products. Banks increasingly co-create offerings with insights from these segments, using historical uptake patterns and attrition signals. Internal benchmarks suggest that data-driven micro-segmentation can improve conversion and retention in vulnerable cohorts.

What makes this commercially valuable is orchestration. Customer lifetime value (CLV) can be optimized through data-informed timing, channel, and messaging strategy. In parallel, anonymized segment insights can be packaged into syndicated retail analytics or sold via data exchanges, creating a secondary monetization stream while remaining compliant with privacy frameworks.

2. Lending risk models

Banks are reengineering risk models using behavioral data from account activity, real-time transaction categorization, open banking inputs, and third-party data (e.g., payroll APIs, gig economy platforms). These models support more granular risk pricing, dynamic limit management, and predictive early-warning systems.

One of the most impactful applications is in underserved segments, such as thin-file borrowers or SMEs with limited collateral. Behavioral data (e.g., payment cadence, recurring income, utility payments) is used to model affordability and payment resilience. In some cases, alternative models of data monetization in banking improve predictive accuracy over legacy scorecards.

These proprietary models are becoming data products in themselves. Several Tier 1 banks now offer API-based credit assessments to fintech lenders or embedded finance providers. Others offer "credit score as a service" to B2B partners, built on fully governed pipelines with explainability layers to meet regulatory auditability.

3. Data-as-a-service platforms

For many banks, shifting from using data to offering data opens a new monetization tier. Data-as-a-service (DaaS) allows financial institutions to productize their internal insights as governed, high-value assets for external stakeholders.

At the core are anonymized, aggregated datasets, such as transaction volumes by merchant type, regional spending trends, or sector-specific credit flows that are packaged and sold to analytics firms, retailers, investors, and even government agencies. These curated datasets serve as strategic intelligence sources for clients conducting market research, location planning, or benchmarking exercises.

More advanced banks have launched self-service data marketplaces that offer real-time access to these insights via APIs or subscription portals. Built-in governance layers, covering consent management, data lineage, and licensing, help ensure regulatory alignment while scaling data product delivery.

Collaborative data utilities are also emerging, where multiple institutions pool datasets to tackle systemic challenges like SME credit risk or payment fraud. These alliances enhance data coverage while sharing the cost and responsibility of governance and platform upkeep.

4. Internal use: cost reduction and operational improvement

Not all data monetization banking is external. Some of the most impactful gains come from applying analytics to internal processes to reduce cost, mitigate risk, and unlock latent efficiency. These savings may not show up as direct revenue but materially improve operating margin and return on assets.

At the branch and back-office level, behavioral and transactional data inform everything from staffing models to cash handling logistics. Forecasting algorithms help treasury teams better predict liquidity needs, optimize hedging, and prevent overexposure to currency or interest rate swings. Even minor improvements in high-volume institutions can translate to millions in annual value.

Data-driven behavioral routing is used in customer service and onboarding flows to lower call center load and improve NPS. Banks can pre-empt issues or auto-route customers to preferred channels by analyzing past interactions and channel preferences, dramatically reducing operational overhead. On the credit side, integrating behavioral models into early decisioning reduces delinquency rates, increases acceptance among lower-risk segments, and narrows loss given default.

Data also enables predictive lifecycle engagement. If a customer closes a mortgage, will they likely need wealth planning next? Is there an upsell opportunity for FX services if a corporate account's spending increases? These signals are often hidden in plain sight until stitched together through intelligent data orchestration.

5. API enabled monetization models

The commercialization of APIs marks one of the most tangible shifts in how banks approach data monetization. APIs are evolving into structured, monetized products that create value for internal teams and ecosystem partners.

Modern banks are launching API marketplaces where partners, fintechs, insurers, and digital platforms can access real-time account, transaction, credit, or identity data under secure, consent-driven conditions. These marketplaces are built with fine-grained access tiers and usage-based pricing, enabling recurring revenue from data interactions that were once locked behind legacy infrastructure.

More strategically, ecosystem monetization is taking root. Banks enable embedded finance use cases by exposing behavioral data streams to trusted partners, such as spend categories, recurring income signals, or cash flow trends. For example, a digital insurer might integrate transaction data to price coverage, or a credit platform might adjust loan offers in real time based on API-derived affordability scores. In both cases, the bank captures a share of the value via access fees or revenue-sharing agreements.

Banks invest in usage analytics to optimize these models, tracking how APIs perform in downstream workflows and using that intelligence to inform bundling, rate cards, and SLA models.

Harness predictive analytics in banking—get the complete guide now!

Success!

Discover how to build an effective data monetization strategy

What makes data monetization in banking different from other industries?

Why can't banks apply the same data monetization strategies in retail, media, or telecom? Unlike other industries, financial institutions operate under complex regulatory, ethical, and operational constraints that shape every data-driven initiative. Data monetization in banking opportunities do exist, but they require a structurally different approach.

Regulatory environment

The financial sector is already among the most active in data monetization, but it does so under some of the world's strictest data protection laws. Regulations such as the EU's General Data Protection Regulation (GDPR) and the Payment Services Directive 2 (PSD2) fundamentally influence how banks can handle, process, and commercialize customer data.

- GDPR enforces stringent requirements for data fairness, purpose limitation, and accountability. Every monetization initiative must demonstrate lawful processing, clear consent, and the ability to trace decisions back to source data and logic.

- PSD2 introduced new obligations and opportunities by requiring banks to provide standardized API access to customer data, with the customer's explicit consent. While this has created the foundation for open banking ecosystems, it has also raised the bar for how data access and usage must be managed, audited, and secured.

- In Canada, Quebec's Bill 64 and similar state-level regulations in the US mirror these trends. They focus heavily on automated decision-making, requiring organizations to disclose when personal data is used in profiling or monetization. Financial institutions must comply with shifting privacy rules and ensure that their decision-making systems are transparent, explainable, and justifiable.

These regulations mean data monetization banking strategies cannot be separated from banks' risk management and compliance architecture. Every new use case must pass through legal, security, and governance review.

Compliance

While many view regulation as a barrier, it can also become a competitive advantage. Banks that invest early in frameworks for data traceability, explainability, and bias mitigation are in a stronger position to develop monetizable products and partnerships. These internal capabilities, including decision audit trails, real-time governance monitoring, and privacy-first data architecture, become prerequisites for secure ecosystem collaboration.

For instance, financial institutions that meet compliance standards faster can become data providers to insurers, retailers, or public agencies through analytics subscriptions, benchmarking reports, or secure APIs.

Ethics

Ethical considerations in banking data monetization go beyond consent forms or compliance checklists. With the rise of generative AI, automated decision-making, and data-driven personalization, regulators and the public are raising questions about fairness, accountability, and transparency.

This aspect makes ethical design a practical requirement. For instance, if an AI model determines loan eligibility or flags fraud, the bank must be able to explain the logic, prove the decision is free of bias, and offer recourse. These demands apply to any monetization initiative that uses customer data to influence outcomes or behavior.

Read also about: Retail data monetization: why it’s worth it and how to do it effectively

How to address key risks in banking data monetization

Monetizing financial data brings commercial opportunity and exposes banks to heightened regulatory, ethical, and operational risks. Missteps can lead to compliance penalties, reputational damage, or wasted investments. At N-iX, we help banking institutions anticipate and address these risks early. Here's how we approach the most pressing categories of risk.

Reputational risks

Trust is not automatically granted, particularly when financial institutions work with personal data at scale. It calls for visible, well-structured practices that put user rights and transparency at the center. To support our clients in building trust from the ground up, N-iX focuses on:

- Embedding consent management and transparency workflows into the architecture of each data product, ensuring that customers are always aware of how their data is being used.

- Applying Privacy by Design principles to product and system development, treating privacy as a structural component.

- Enabling secure data monetization by using anonymization and synthetic data techniques that maintain utility while eliminating exposure risks.

Legal and regulatory risks

Financial data monetization doesn't happen in a vacuum. Banks operate within a dense local and international regulations landscape, including GDPR, PSD2, and emerging AI and privacy laws. Failing to align with these standards can bring more than fines; it can halt initiatives and damage institutional credibility. To support our partners in staying compliant and audit-ready, we apply the following practices:

- Involving legal and compliance teams early in the use case design phase to ensure monetization aligns with regulatory frameworks before any implementation begins.

- Implementing governance architectures that support traceability, bias mitigation, explainability, and data lineage.

- Maintaining robust audit trails for data access, especially in open banking environments governed by API-based sharing.

- Adapting monetization models to regional constraints, including sovereign data laws and cross-border transfer rules.

Business risks

Many data monetization projects underperform not because of poor technology, but because they lack a clear value hypothesis or measurable success criteria. Without business alignment and strong operational grounding, even promising initiatives lose momentum. N-iX mitigates this execution risk by helping clients:

- Frame each use case with business outcomes in mind, applying hypothesis-driven validation before scaling to larger audiences or ecosystems.

- Run controlled pilot programs tied to specific ROI metrics, such as customer lifetime value uplift, product cross-sell, or ecosystem monetization potential.

- Align teams early through steering committees, ensuring that legal, product, finance, and data leaders have shared ownership over outcomes and risks.

Organizational risks

Data monetization in banking doesn't work without integration between systems, business units, and teams. Many banks struggle with data fragmentation, conflicting priorities across departments, and unclear accountability for monetization outcomes. These internal misalignments often delay or derail initiatives. To help banks create the operational foundation for scalable monetization, we:

- Conduct end-to-end data readiness assessments that identify technical and organizational blockers across business units.

- Design modular data product architectures that work across silos while respecting domain-specific requirements.

- Establish clear operating models for monetization, including budgeting, cost recovery, and business-side accountability, often supported by FinOps principles to manage financial visibility.

In summary

Data monetization isn't a mandatory initiative, but it's one of the few levers that can directly grow revenue without raising costs. The business case is clear for banks already sitting on years of rich, underused customer and transaction data: turn that data into actionable insight, more innovative products, and entirely new revenue streams.

With deep experience in data engineering, AI, and secure cloud infrastructure, N-iX works with financial institutions to structure, operationalize, and scale data monetization initiatives. From building secure data platforms to developing commercial-grade data products, we help banks move from data-rich to data-smart safely, efficiently, and at enterprise scale.