Digital Twins for Logistics: Smarter, More Resilient Supply Chains

What a logistics digital twin really is, the four twin types that matter, how they are built, and how to use s...

How AI supercharges embedded finance: the BaaS stack, contextual underwriting, real-time risk, agentic finance, a reference architecture, regulation, and an implementation roadmap.

Embedded finance AI is the use of artificial intelligence to deliver financial products inside non-financial customer journeys, so that lending, payments, insurance, and accounts appear at the exact moment a user needs them and are underwritten, priced, and risk-checked in real time. Embedded finance puts the financial product where the demand already is, at the point of sale, inside a logistics app, on a marketplace, and AI is what makes those embedded products contextual, instant, and economically viable at scale.

The shift is already reshaping the market. Embedded finance has moved from a niche feature to a primary distribution channel for financial services, with industry analysts valuing the global market in the low hundreds of billions of dollars in 2025 and projecting double-digit annual growth through the end of the decade. The story of 2025 was platforms capturing the customer-facing value chain while banks increasingly supplied the regulated infrastructure behind the scenes. Apple folded Klarna into Apple Pay, Amazon deepened its Affirm partnership for checkout credit, Shopify extended capital and balances to merchants using live sales data, and Tesla priced auto insurance from real-time vehicle telemetry. None of those experiences work without AI doing the contextual decisioning underneath.

This guide is written for fintech CTOs and CPOs, bank heads of digital, and platform product leaders. It explains what embedded finance is and the banking-as-a-service (BaaS) stack that enables it, where AI adds the most value, the reference architecture that ties APIs, data, and AI services together, real-world examples across lending, insurance, and payments, the regulation and risk you must design for, a phased implementation roadmap, the ROI case, the common pitfalls, and a set of executive recommendations. The aim is an architecture-level mental model you can act on, not a vendor pitch.

Key Takeaways

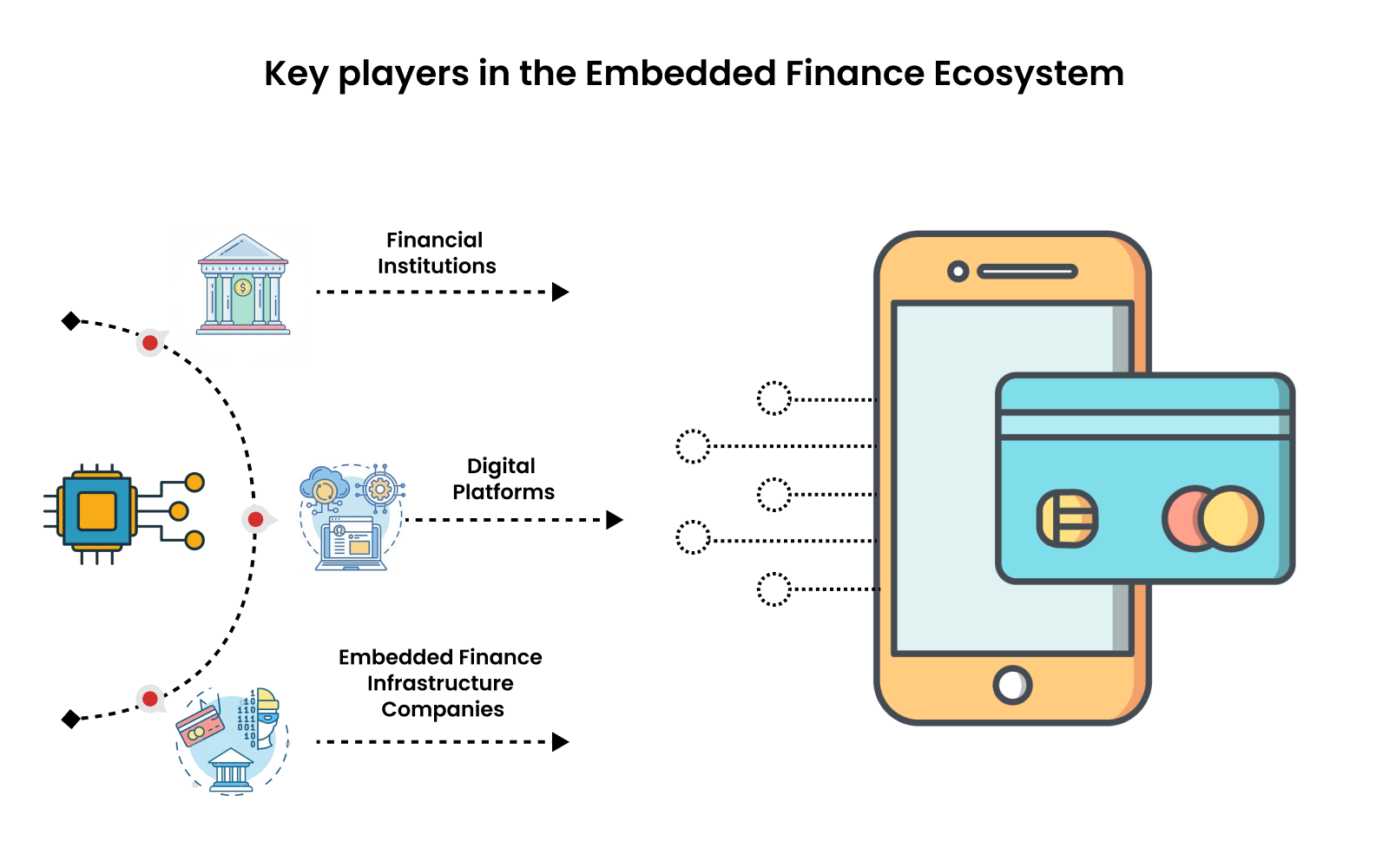

Embedded finance is the integration of financial services into the products and journeys of non-financial companies, so the customer never leaves the host experience to transact, borrow, pay, or insure. A ride-hailing app offering its drivers instant earnings access, a marketplace extending working-capital loans to sellers, a travel site adding trip insurance at checkout, these are all embedded finance. The financial product becomes a feature of the journey rather than a separate destination.

Underneath it sits the banking-as-a-service (BaaS) stack, which separates the regulated capability from the customer-facing brand. It typically has three roles:

The categories of product that get embedded are consistent across the industry: embedded payments (pay-in and pay-out inside the app), embedded lending (point-of-sale credit, BNPL, merchant cash advance, working capital), embedded accounts and cards (wallets, branded debit, expense cards), and embedded insurance (cover offered contextually at checkout). The 2025 market made one thing clear: the value increasingly accrues to whoever owns the customer journey and the data, while the regulated bank becomes the back end. That is precisely why AI matters, because the journey owner needs to make a sound financial decision in milliseconds, with the data the moment provides.

Embedded finance needs AI because the embedded moment is fast, data-rich, and unforgiving. A traditional financial product can take days to underwrite and tolerate paperwork; an embedded product has to decide in the time it takes a checkout page to load, using whatever context the host journey supplies, while still being profitable and compliant. That is an AI problem.

Three properties of the embedded moment make AI essential rather than optional:

In short, the BaaS stack delivers the plumbing; AI delivers the intelligence that makes an embedded product contextual, instant, and economic. The rest of this guide is about where that intelligence pays off and how to build it responsibly.

AI adds the most value at six points in the embedded-finance lifecycle: contextual underwriting and embedded lending, real-time risk and fraud, hyper-personalized offers and next-best financial action, automated KYC and onboarding, compliance automation, and conversational or agentic finance. Each maps to a concrete model capability and a measurable business outcome.

AI underwrites embedded credit using alternative, real-time data from the host journey rather than relying on a thin or stale credit file. A marketplace can extend a seller a working-capital loan priced off live sales velocity, payouts, and return rates; a checkout can offer BNPL underwritten on cart composition, device, and behavioral signals. Machine-learning models combine traditional bureau data with this contextual signal to approve more good customers, price risk individually, and do it instantly. Shopify Capital, for example, offers merchants credit based on real-time platform data and collects repayment as a share of daily sales, an underwriting model that only works because the data and the decision are both continuous.

AI scores every embedded transaction, application, and account event for fraud and risk in sub-second windows. Because embedded finance multiplies the number of entry points (every distributor is a new front door), fraud and synthetic-identity risk rise, and real-time scoring is the only viable defense. The same streaming-and-model foundations covered in real-time AI fraud detection for financial institutions apply directly here: supervised models for known patterns, anomaly detection for novel attacks, graph analytics for fraud rings across distributors, and behavioral biometrics for account takeover.

AI decides which financial product to surface, to whom, and when, so the offer feels like help rather than an interruption. Instead of showing every user the same credit line, models predict need and propensity from in-journey behavior and recommend the next-best financial action, a savings nudge, a card upgrade, a top-up, an insurance add-on, at the moment it is most relevant and least intrusive. Done well, personalization lifts conversion and customer lifetime value; done poorly, it becomes spam, which is why the targeting model and the suppression logic matter as much as the offer.

AI compresses know-your-customer (KYC) onboarding from days to seconds by automating identity verification, document extraction, liveness checks, and risk screening. Embedded products live or die on friction, and a multi-step manual onboarding kills conversion. Computer vision reads and validates documents, biometric checks confirm a live human, and machine-learning screening flags sanctions and politically-exposed-person hits, all orchestrated into a single in-flow step. The same models reduce false rejections that would otherwise lose legitimate customers.

AI helps embedded-finance operators keep up with regulatory obligations at scale: transaction monitoring for AML, automated suspicious-activity detection, adverse-media screening, and assistance with disclosures and reporting. Large language models grounded in current regulation and internal policy can help compliance teams interpret rules, draft documentation, and triage alerts, provided they are constrained to verified sources. Grounding those assistants in authoritative internal data through enterprise RAG systems is what keeps the output reliable and auditable rather than a hallucination risk.

AI is moving from scoring decisions to taking actions. Conversational interfaces let users apply for credit, query a balance, or buy cover in natural language inside the host app. The next step is agentic finance, where AI agents execute multi-step financial tasks, reconcile, move funds between accounts, optimize a payment, initiate a claim, under defined policy and human oversight. This is an emerging frontier rather than a solved one, and it inherits all the control requirements explored in agentic AI in banking and autonomous financial operations. For embedded finance, the promise is financial products that do not just appear in context but act on the user's behalf within guardrails.

| AI use case | What it does | Key data / model | Primary outcome | Main risk to manage |

|---|---|---|---|---|

| Contextual underwriting / embedded lending | Approves and prices credit in real time from in-journey data | Bureau + alternative data; gradient-boosted / ML models | Higher approval rates, instant credit, individualized pricing | Fair-lending bias, explainability |

| Real-time risk & fraud | Scores every event for fraud across all distributors | Streaming events; supervised, anomaly, graph models | Lower fraud losses, fewer false declines | False positives, model drift |

| Personalized offers / next-best action | Surfaces the right product at the right moment | Behavioral + journey data; propensity models | Higher conversion and lifetime value | Intrusiveness, suppression logic |

| Automated KYC / onboarding | Verifies identity and screens risk in-flow | Computer vision, biometrics, screening models | Seconds-not-days onboarding, less drop-off | False rejections, privacy |

| Compliance automation | Monitors transactions, screens, assists reporting | AML models; LLMs grounded via RAG | Scalable compliance, fewer missed alerts | Hallucination, accountability |

| Conversational / agentic finance | Lets users transact in natural language; agents act under policy | LLMs, tool-use agents, orchestration | Frictionless UX, automated tasks | Autonomy guardrails, auditability |

The reference architecture has three layers, a BaaS/API layer, a real-time data layer, and an AI services layer, bound together by an end-to-end governance and security plane. Thinking in these layers keeps the build modular and makes clear where regulated capability ends and intelligence begins.

This is the regulated foundation. It exposes the licensed capabilities, accounts, card issuing, payments, lending, insurance, through clean APIs, and includes the ledger, the connections to licensed partners, and the orchestration that turns a product decision into a real money movement. The distributor integrates here. The defining principle is that the API layer abstracts regulatory complexity without abstracting away regulatory responsibility.

Embedded-finance AI is only as good as the data it can act on in the moment. This layer ingests events from the host journey and the financial rails (transactions, applications, telematics, sales, behavior) through a streaming backbone, and serves them to models via a feature store that provides both fresh real-time features and historical context with low latency, using identical definitions in training and production. It is also where consented data from the distributor is unified with the institution's own data. Without this layer, contextual decisioning is impossible, the models simply will not have the signal.

This is the intelligence: the underwriting models, fraud and risk scoring, personalization and next-best-action engines, KYC and document AI, compliance models, and conversational or agentic services. These are exposed as services the decisioning flow calls in real time, with strict latency budgets and graceful degradation so a slow signal never blocks the whole decision. Increasingly this layer also hosts LLM-based assistants and agents, grounded in verified data and constrained by policy.

Cutting across all three layers is governance: model risk management, explainability, bias testing, audit logging, data privacy and consent, and access control. In financial services this is not an overlay added at the end; it is a design constraint from day one, and it is the subject of AI governance in financial services. The institutions that scale embedded finance treat governance as the enabler that lets them ship models confidently rather than a brake.

Real-world embedded finance spans lending, payments, insurance, and accounts, and the most successful examples share one trait: an AI decision made on contextual data at the point of need. A few illustrative patterns:

The common thread is that AI is what turns a generic financial product into a contextual one, priced and approved for this user, in this moment, on this journey.

Embedded finance is regulated through the licensed institution behind the product, and embedding a financial service into a non-financial journey does not move the regulatory obligation, it stays with the licensed provider, while the distributor and BaaS platform carry significant operational and reputational responsibility. This is the single most misunderstood point in the category, and getting it wrong is how programs fail compliance reviews.

The obligations that embedded-finance AI must design against include:

The practical posture is compliance-by-design: bake explainability, bias testing, audit logging, and clear accountability between distributor, BaaS platform, and licensed provider into the architecture from the start, rather than retrofitting them after launch.

Build in phases, proving a single embedded product on a contained scope before expanding, rather than attempting to launch a full financial suite at once. A staged approach de-risks the program, produces early wins, and lets governance mature alongside the product.

Choose the one embedded product with the clearest demand and best data (often embedded payments or a single lending product). Select your BaaS and licensed partners, define the accountability split between distributor, platform, and provider, and stand up the real-time data layer, event streaming and a first feature store. Set target metrics up front: conversion, approval rate, fraud and default rate, onboarding completion, and unit economics.

Ship the first product with AI decisioning, often running new models in shadow mode alongside conservative rules before they take live decisions, automated KYC onboarding, and real-time fraud scoring. Start with score-and-review or graduated friction rather than fully automated approvals, and wire the feedback loop so confirmed outcomes (repayments, chargebacks, fraud, claims) flow back into training.

Layer in personalization and next-best-action, refine contextual underwriting with the data you have now accumulated, and add a second embedded product. Begin orchestrating signals (risk, fraud, propensity) into unified decisions rather than running each in isolation, and stand up the model-operations dashboards and drift monitoring that will run for the life of the system.

Expand across distributors and products, formalize model-risk documentation and validation, introduce conversational interfaces, and, where controls justify it, selectively pilot agentic workflows for well-bounded tasks. By this stage the program is a living system with clear ownership, monitoring, and a documented governance posture.

Most teams blend approaches. BaaS platforms and point vendors accelerate the regulated rails and common AI components; in-house engineering matters where the embedded product depends on proprietary journey data and a differentiated experience. The hard parts, the real-time data layer, the feature store, model operations, and the integration of AI services into a sub-second decision flow, are specialized AI engineering work. This is where many product leaders bring in a dedicated AI development partner. As an enterprise AI engineering and data transformation partner, Mind Supernova helps fintechs, banks, and platforms design and build the real-time data pipelines, decisioning services, and MLOps foundations that contextual embedded products depend on, while the institution retains ownership of product strategy and risk policy.

The ROI comes from four sources, new revenue, higher conversion and approval rates, lower fraud and default losses, and lower onboarding and operating cost, weighed against the build and ongoing model-operations cost. For platforms that already own a high-intent audience, the revenue case is often the largest line.

Frame the business case around these levers:

The discipline that matters is measuring the full picture: revenue gained, plus losses avoided, plus cost removed, against build and model-operations cost. A program optimized only for approval volume will leak fraud and defaults; one optimized only for caution will throttle the revenue that justifies the build. The right metric is total contribution, and well-built embedded-finance AI moves it up while keeping risk in check.

Most embedded-finance AI programs underperform for predictable reasons rather than because the idea was wrong:

For product, technology, and digital leaders setting direction on embedded finance, the priorities are clear:

Embedded finance AI is the use of artificial intelligence to deliver financial products, lending, payments, accounts, and insurance, inside non-financial customer journeys, with underwriting, pricing, risk checks, and personalization happening in real time. The banking-as-a-service stack moves the product to where demand already is, and AI makes each embedded product contextual, instant, and economically viable at scale.

AI improves embedded lending by underwriting credit in real time on contextual, in-journey data, such as a merchant's live sales or a buyer's checkout behavior, rather than relying only on a static credit file. This lets lenders approve more good customers instantly, price risk individually, and offer credit at the exact point of need, as with platform capital advances repaid from daily sales.

Banking as a service is a model where licensed banks expose their regulated capabilities, accounts, card issuing, payments, and lending, through APIs so that non-financial companies can embed financial products without holding a banking license themselves. A BaaS or middleware platform sits between the licensed provider and the distributor, handling integration, ledgering, and compliance tooling.

It has three layers: a BaaS/API layer that exposes licensed financial capabilities, a real-time data layer (event streaming and a feature store) that supplies fresh and historical context, and an AI services layer (underwriting, fraud, personalization, KYC, compliance, and conversational or agentic services). A governance and security plane, covering model risk, explainability, privacy, and audit, cuts across all three.

Yes. Embedding a financial product does not move the regulatory obligation; the licensed institution behind it remains accountable, while distributors and BaaS platforms carry significant operational responsibility. Fair lending, KYC and AML, model-risk management (such as SR 11-7), data privacy, and product-specific rules all apply, and BNPL in particular is being brought fully under FCA regulation in the UK.

Agentic finance is the emerging use of AI agents that take multi-step financial actions, moving funds, optimizing a payment, initiating a claim, on a user's behalf within defined policy and human oversight, rather than only scoring decisions or answering questions. In embedded finance it points toward products that not only appear in context but act for the user inside guardrails, and it inherits the strict control and auditability requirements of agentic AI in banking.

A phased program typically shows initial value within a few months. A common pattern is strategy, partners, and data foundations in the first three months, a first product live with AI in the loop by around six months, added intelligence and a second product by twelve months, and broader scaling and governance hardening beyond that. Timelines depend on partner selection, data readiness, and regulatory complexity.

Embedded finance has shifted the distribution of financial products to wherever demand already lives, and AI is the layer that makes those embedded products contextual, instant, and economic. The winners are not simply the ones who bolt a lending or payments API onto a checkout; they are the ones who pair the BaaS stack with a serious real-time data layer and well-governed AI services, contextual underwriting, real-time risk and fraud, personalization, automated onboarding, compliance automation, and, carefully, conversational and agentic capabilities. Done well, this opens new revenue, lifts conversion, lowers losses, and deepens the customer relationship, all while keeping the regulator satisfied.

The strategic decisions, which products to embed, how much risk to take, and where to set the experience-versus-control balance, must stay with your product and risk leadership. But the engineering underneath, the real-time data pipelines, decisioning services, model operations, and integration, is specialized work that many teams accelerate with an experienced AI engineering and data transformation partner. If embedded finance is on your roadmap, the most useful next step is an honest assessment of your data and decisioning readiness against the architecture described here, followed by a contained pilot on a single product that proves the economics before you scale.

What a logistics digital twin really is, the four twin types that matter, how they are built, and how to use s...

How computer vision transforms physical retail: the enabling tech, use cases from shelf compliance to checkout...

How AI demand sensing and IoT move supply chains from reactive forecasting to autonomous, closed-loop decision...