AI Customer Journey Optimization: Personalizing Retail at Scale

How retailers use AI to personalize the end-to-end customer journey at scale: the enabling stack, use cases, m...

A practical guide to real-time AI fraud detection for banks, fintechs, and payment firms: streaming architecture, model types, false-positive reduction, and ROI.

Real-time AI fraud detection is the use of machine learning models to score every transaction, login, and account event the moment it happens, blocking or flagging suspicious activity within a sub-second window before money moves. Unlike older systems that batch-review activity hours or days later, a real-time approach decides while the customer is still in the flow, which is the only point at which most modern fraud can actually be stopped.

The shift is not optional. Fraud has industrialized. Industry estimates put global fraud losses at roughly $442 billion in 2025, and the attackers are now using the same generative AI, automation, and global coordination that defenders are. Feedzai's 2025 reporting found that around 90% of financial institutions already use AI for fraud detection, and that the overwhelming majority believe fraudsters are using generative AI against them. The arms race is live, and rules-only defenses are losing it.

This guide is written for Heads of Fraud and Risk, CISOs, and CTOs at banks, fintechs, and payment companies. It covers why rule-based systems fail, the streaming architecture that makes sub-second scoring possible, the model types that matter (supervised, unsupervised, graph, behavioral biometrics, and generative AI), how to reduce false positives without letting fraud through, the model-operations and regulatory discipline this all requires, a phased build roadmap, and the ROI math that justifies the investment. The goal is to give you an architecture-level mental model you can act on, not a vendor pitch.

Key Takeaways

Rules-only fraud systems fail because they encode yesterday's fraud, react slowly to new patterns, and generate too many false alarms. A rule like "flag any transaction over $5,000 from a new device in a high-risk country" is transparent and easy to reason about, which is exactly why fraudsters defeat it. They probe the boundaries, learn the thresholds, and structure their activity to slip underneath, splitting a large theft into many small payments that each look ordinary.

Three structural problems make a rules-only posture untenable for a modern financial institution:

This is not an argument to throw rules away. Rules remain valuable for hard policy constraints, regulatory blocks, and explainable last-mile controls. The point is that rules must become one layer in a system whose intelligence comes from machine learning, not the whole defense.

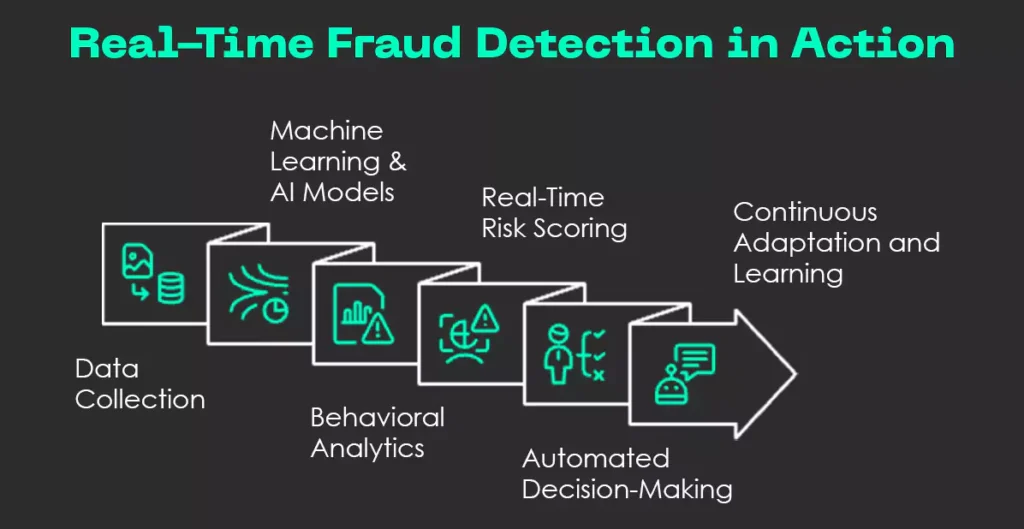

A real-time fraud detection system is a streaming pipeline that ingests events, enriches them with fresh and historical features, scores them with one or more models in milliseconds, and routes the decision to allow, block, challenge, or review. The models get the attention, but the architecture around them determines whether sub-second decisioning is even possible.

Everything starts with a durable, high-throughput event stream. Transactions, authentication events, device signals, and account changes flow through a streaming backbone (commonly built on technologies such as Apache Kafka, Apache Flink, or managed cloud equivalents). Streaming, rather than batch, is what lets the system react to an event as it occurs rather than in a nightly job. For a payments business processing thousands of events per second, the stream must be partitioned, ordered where it matters, and resilient to spikes.

Models are only as good as the features they see at decision time. A feature store is the component that computes, stores, and serves features consistently. It solves two hard problems at once. First, it provides real-time features, for example "how many transactions has this card made in the last 60 seconds" or "velocity of new payees added this hour," computed on the live stream. Second, it provides historical features such as the customer's 90-day spending baseline, all served with low latency. Critically, the feature store ensures the same feature definitions are used in training and in production, eliminating the train-serve skew that silently degrades many fraud models.

When an event arrives, the scoring layer assembles its features, runs them through the model ensemble, and returns a risk score within a strict latency budget, typically tens to low hundreds of milliseconds end to end, because the payment or login is waiting on the answer. Achieving this consistently requires careful engineering: pre-computed features, optimized model serving, and graceful degradation so that if one signal is slow, the decision still completes. The output is not always a binary block. Mature systems return a calibrated risk score that feeds a decision policy: allow, soft-challenge (step-up authentication), hard-block, or queue for human review.

The final piece is the loop that makes the system smarter over time. Confirmed fraud, customer disputes, chargebacks, and analyst dispositions feed labels back into training data. A well-built pipeline treats this feedback as a first-class data product, because the speed and quality of your labels directly cap how fast your models can adapt to new fraud. This same event-driven, streaming foundation is what increasingly powers agentic AI in banking and autonomous financial operations, where systems do not just score risk but initiate the follow-up actions a human analyst would otherwise perform.

Modern fraud detection layers several model families, because each catches a different kind of fraud and no single technique covers the threat surface. The strongest programs run an ensemble and orchestrate the signals together.

Supervised models learn from labeled examples of fraud and legitimate activity. Gradient-boosted decision trees (such as XGBoost and LightGBM) remain workhorses because they are accurate, fast to score, and reasonably interpretable; deep neural networks are used where data volume and complexity justify them. Supervised models excel at catching variations of known fraud patterns. Their weakness is structural: they can only learn fraud that has already been labeled, so they lag genuinely novel attacks.

Unsupervised models flag activity that deviates from normal behavior without needing fraud labels. Techniques such as isolation forests, autoencoders, and clustering build a picture of "normal" for an account, a merchant, or a population, then surface outliers. This is how you catch new fraud patterns the moment they emerge, before you have enough confirmed cases to train a supervised model. The trade-off is more noise, so anomaly scores are usually one input to a broader decision rather than an automatic block.

Graph analytics models the relationships between entities, accounts, devices, phone numbers, addresses, and payees, rather than looking at transactions in isolation. This is the decisive technique against fraud rings, mule networks, and synthetic identities, because the fraud signal lives in the connections. When dozens of "unrelated" accounts share devices, funnel money through common nodes, or form suspicious community structures, a graph reveals the pattern that transaction-level models miss. Feedzai has reported a sharp rise in fraud-ring activity, and graph-based detection, including graph neural networks, has become a core part of the modern stack precisely because coordinated fraud is now a dominant loss driver.

Behavioral biometrics analyzes how a user interacts, typing rhythm, mouse movement, touch pressure, device-holding angle, and navigation patterns, to build a behavioral signature. It is especially powerful against account takeover and authorized push payment (APP) scams, where the credentials are legitimate but the behavior is not. Hesitation patterns and on-screen coaching signatures can indicate a customer being socially engineered in real time, allowing an intervention before the payment completes.

Generative AI cuts both ways. On defense, large language models help analysts by summarizing cases, drafting narrative reports, querying data in natural language, and synthesizing rare fraud scenarios to strengthen training data. On offense, generative AI has industrialized attacks. Industry surveys in 2025 found that the large majority of financial institutions believe fraudsters are using generative AI, with deepfake-enabled scam reports rising several-fold year over year and the cost of producing a convincing deepfake clip falling to a few dollars. This is why static defenses fail and why detection must combine many independent signals: a deepfake may beat a face check but still fail the behavioral, device, and network signals around it. For institutions deploying LLMs in their own fraud and risk workflows, grounding those models in verified internal data through approaches like enterprise RAG systems is essential to keep the assistance reliable and auditable.

| Model type | Best at catching | Needs labels? | Real-time fit | Explainability | Key limitation |

|---|---|---|---|---|---|

| Supervised (boosted trees, neural nets) | Known and varied fraud patterns | Yes | High | Moderate (with SHAP) | Misses genuinely novel fraud |

| Unsupervised / anomaly | New, emerging, zero-day fraud | No | High | Lower | Higher noise / false positives |

| Graph / network analytics | Fraud rings, mules, synthetic identity | Optional | Medium to high | Moderate (visual) | Heavier infrastructure |

| Behavioral biometrics | Account takeover, APP / scam coaching | Mostly no | High | Moderate | Needs rich interaction data |

| Generative AI (LLMs) | Analyst augmentation, scenario synthesis | N/A | Assistive | Variable | Hallucination / must be grounded |

You reduce false positives by replacing blunt rules with calibrated risk scores, adding context from more signals, and using friction proportionally instead of blocking outright. The objective is not the lowest possible fraud rate at any cost; it is the best balance between fraud losses and the cost of declining good customers. Both sides of that equation are real money.

Practical levers that consistently move the false-positive rate down:

The payoff is well documented in the field. Institutions that move from rules-heavy systems to advanced AI commonly report 40-60% reductions in false positives while maintaining or improving fraud catch rates; widely cited examples include large banks reporting roughly a 50% drop in false positives alongside materially better detection after adopting machine learning. For a high-volume institution, even a few percentage points of false-positive reduction translates into millions in recovered revenue and lower operating cost.

Production fraud models require continuous monitoring, drift detection, and disciplined retraining, because fraud is a non-stationary problem: the distribution shifts as fraudsters adapt. A model that was excellent last quarter can quietly decay. Treating fraud models as deploy-once assets is one of the most common and expensive mistakes.

A sound model-operations practice includes:

This is mature MLOps applied to an adversarial domain, and it is where many fraud programs underinvest. The models are often the easy part; the monitoring, retraining, and label infrastructure are what keep them effective in production.

Explainability and regulation are not afterthoughts in financial-services fraud AI; they are design constraints. A model that cannot explain why it blocked a transaction creates operational, customer, and regulatory risk all at once. Analysts need a reason to action a case, customers are entitled to understand adverse decisions, and supervisors expect models to be governed.

The core regulatory anchors that fraud and risk leaders should design against include:

The practical answer is explainable AI tooling. Techniques such as SHAP and LIME generate per-decision feature attributions, giving analysts the reason codes and giving model-validation teams the evidence regulators expect. Fraud sits inside the broader discipline of AI governance in financial services, which is where the model-risk, fairness, and compliance requirements that constrain a fraud program are defined and enforced. Treating governance as an enabler rather than a blocker is what lets you ship fraud models confidently.

Build in phases, proving value on a contained scope before expanding, rather than attempting a big-bang replacement of the entire fraud stack. A staged approach de-risks the program, builds organizational confidence, and produces measurable wins early.

Establish the streaming backbone and a first feature store, and stand up a baseline supervised model running in shadow mode alongside your existing rules. Shadow mode lets you measure what the model would have done without taking live decisions, which builds trust and surfaces data-quality issues early. Define your target metrics up front: detection rate, false-positive rate, and the dollar value of both fraud losses and false-positive friction.

Move the model into the live decision path for one product or channel, starting with score-and-review or step-up authentication rather than hard blocks. Wire up the feedback loop so confirmed outcomes flow back into training. Establish the model-operations dashboards and drift monitoring that will run for the life of the system.

Add the techniques that cover your gaps: anomaly detection for emerging fraud, graph analytics for rings and mule networks, and behavioral biometrics for account takeover and scam coaching. Begin orchestrating signals into a unified risk decision rather than running each in a silo.

Expand across products and channels, automate retraining with validation gates, formalize SR 11-7-aligned model documentation and validation, and selectively introduce automation or agentic workflows for case handling where the controls justify it. By this stage the program is a living system with clear ownership, monitoring, and a documented governance posture.

Most institutions blend approaches. Vendor platforms accelerate time to value for common patterns; in-house engineering matters where fraud intersects with proprietary data and customer experience. The hard parts, the streaming pipeline, the feature store, model operations, and integration, are specialized AI engineering work. This is where many institutions bring in a dedicated AI development partner. As an enterprise AI engineering partner, Mind Supernova helps banks, fintechs, and payment firms design and build the streaming detection pipelines, feature stores, and MLOps foundations that real-time fraud programs depend on, while the institution retains ownership of fraud strategy and risk policy.

The ROI comes from three measurable sources: fraud losses prevented, false-positive costs reduced, and operational efficiency gained, set against the cost of building and running the system. For most institutions of scale, the fraud-loss and false-positive lines alone justify the investment.

Frame the business case around these levers:

The discipline that matters is measuring both sides of the trade-off. A system tuned only to minimize fraud will over-block and quietly destroy revenue and customer trust; a system tuned only for approval rates will leak fraud. The right metric is total cost, fraud losses plus false-positive friction plus operating cost, and real-time AI moves that total down when it is built and governed well.

Most fraud-AI programs underperform for predictable, avoidable reasons rather than because the models were wrong:

For fraud, risk, and technology leaders setting direction, the priorities are clear:

Real-time AI fraud detection is the use of machine learning models to evaluate each transaction or account event the instant it occurs and decide, within a sub-second window, whether to allow, challenge, block, or review it. It replaces or augments slower, rule-based and batch-review approaches so fraud can be stopped before money moves rather than discovered afterward.

AI learns subtle, evolving patterns from data and adapts as fraud changes, while rule-based systems only encode patterns a human has already written and are easily probed and defeated. In practice, AI systems detect more fraud while producing far fewer false positives, with institutions commonly reporting 40-60% reductions in false alarms after moving to machine learning.

AI reduces false positives by producing calibrated risk scores instead of blunt block/allow rules, by adding context from many independent signals (device, behavior, network, history), and by enabling graduated responses such as step-up authentication for ambiguous cases. This lets institutions decline genuinely risky activity while letting good customers through.

The main families are supervised models (such as gradient-boosted trees and neural networks) for known patterns, unsupervised anomaly detection for new fraud, graph and network analytics for fraud rings and synthetic identities, and behavioral biometrics for account takeover and scams. Generative AI increasingly assists analysts and synthesizes training scenarios. Strong programs combine several.

Banks detect fraud rings with graph and network analytics, which model the relationships between accounts, devices, addresses, and payees rather than looking at single transactions. Coordinated schemes reveal themselves through shared connections and suspicious community structures that transaction-level models cannot see, which is why graph techniques, including graph neural networks, have become central to modern fraud detection.

It can be, when built with governance in mind. Frameworks such as SR 11-7 in the U.S. and the EU AI Act require documented, validated, monitored models with human oversight and, in many cases, explainability. Using explainable AI techniques (such as SHAP and LIME) to produce reason codes, plus disciplined model-risk management, is how institutions keep AI fraud detection compliant.

A phased program typically shows initial value within a few months. A common pattern is foundations and a shadow-mode model in the first three months, a contained live deployment by around six months, additional model types layered in by twelve months, and broader scaling and governance hardening beyond that. Timelines depend on data readiness, transaction volume, and existing infrastructure.

Fraud has become an AI-versus-AI contest, and rules-only defenses cannot keep pace. The institutions pulling ahead treat fraud detection as a real-time machine learning system: a streaming pipeline feeding a feature store, an ensemble of supervised, anomaly, graph, and behavioral models scoring every event in milliseconds, all wrapped in serious model operations and governance. Done well, this stops more fraud, frees good customers from needless friction, and moves total cost down rather than just shifting it.

The strategic decisions, what fraud to prioritize, how much friction to accept, and where to set the risk appetite, must stay with your fraud and risk leadership. But the engineering underneath, the streaming architecture, feature store, real-time scoring, and MLOps, is specialized work that many institutions accelerate with an experienced AI engineering partner. If real-time fraud detection is on your roadmap, the most useful next step is a clear-eyed assessment of your current data and infrastructure against the architecture described here, then a contained pilot that proves value before you scale. For teams weighing how AI reshapes financial products more broadly, the same real-time, data-driven foundations also underpin the shift toward embedded finance and the future of financial products.

How retailers use AI to personalize the end-to-end customer journey at scale: the enabling stack, use cases, m...

A practical engineering and compliance guide to building HIPAA-compliant AI: PHI rules, BAAs for LLM vendors,...

How AI supercharges embedded finance: the BaaS stack, contextual underwriting, real-time risk, agentic finance...