Custom ERP vs Off-the-Shelf Solutions: When SAP and Oracle Are Not the Right Answer

Custom ERP vs off-the-shelf SAP and Oracle: when packaged ERP fails, the composable alternative, and a clear b...

Agent-as-a-service (AaaS) sells completed work, not software seats. Here is how the SaaS-to-AaaS shift rewrites pricing, unit economics, moats, and procurement.

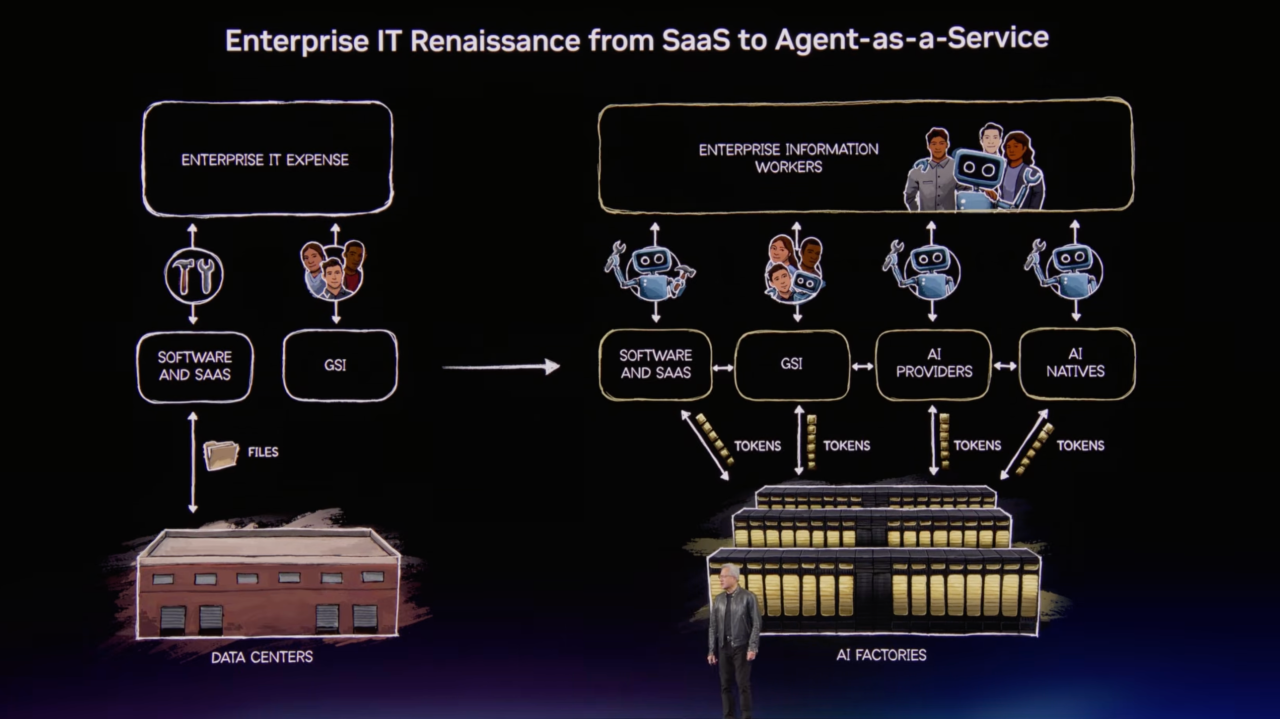

Agent-as-a-service (AaaS) is a software business model in which a vendor sells completed work performed by autonomous AI agents, rather than selling access to a tool that a human operates. The customer does not pay for a login, a seat, or a feature set. They pay for an outcome: a resolved support ticket, a reconciled invoice, a qualified lead, a closed compliance case. The software still exists, but it has receded into the background. What is now for sale is the work itself.

This is a sharper break from traditional Software-as-a-Service than it first appears. SaaS sold capability and charged for access, usually per seat per month. Its core promise was leverage: give a human a better tool and they get more done. AaaS sells the result directly and charges for it, because the agent does the work without a human in the loop on every task. When a single agent can resolve hundreds of cases that previously required a team of licensed users, charging per seat stops describing the value being delivered, and the entire commercial logic of the category starts to bend.

For SaaS founders, product leaders, and the investors who fund them, this is not a feature decision. It is a business-model decision that touches pricing, gross margin, product architecture, defensibility, and go-to-market all at once. For software buyers, it changes procurement, accountability, and the shape of vendor lock-in. This article maps the shift in practical terms: what AaaS is, why it is happening now, how pricing is evolving, what it does to unit economics, where moats come from in an agent world, and what executives on both sides of the table should do about it.

Key Takeaways

Agent-as-a-service is a delivery model where autonomous or semi-autonomous AI agents perform a defined job end to end, and the vendor charges for the completed job rather than for the software that enables it. The simplest way to understand the difference is to ask what the customer is buying. With SaaS, the customer buys a capability and supplies the labor. With AaaS, the customer buys the labor and the capability together, packaged as a result.

Consider customer support. A traditional helpdesk platform charges per agent seat per month. The software organizes tickets, suggests responses, and tracks metrics, but a human resolves each case. An AaaS support product charges per resolved conversation. The agent reads the ticket, retrieves the relevant policy, takes the action, and confirms resolution, escalating to a human only when it cannot proceed. The customer is no longer paying for a tool that ten support reps use. They are paying for resolutions, however many agents or models it takes to produce them.

It is equally important to distinguish AaaS from simply selling raw API access to a model. Reselling tokens from a foundation model is infrastructure, not a product. The customer still has to build the orchestration, the retrieval, the guardrails, the evaluation, and the integration into their systems of record. AaaS sits above that layer. The vendor owns the full loop, including the unglamorous parts: connecting to the customer's data, handling edge cases, measuring whether the work was actually done correctly, and standing behind the result commercially. The difference between an API and an agent product is the difference between selling electricity and selling a finished, guaranteed job. This distinction matters because much of the engineering effort, and most of the defensibility, lives in that gap. Our deeper treatment of how this changes the craft of building software is in AI-powered software development beyond coding assistants.

It helps to place AaaS on a spectrum of how much work the software does versus the human.

Most real products today live somewhere in the middle and are migrating rightward. The strategic question for any software company is not whether to add AI features. It is how far along this spectrum the product should travel, and how fast, given the economics and the trust requirements of its market.

The shift is happening because agents now do work rather than merely enable it, and once software can complete a unit of work and verify it, charging for access stops matching the value created. Three forces converged to make this practical at the same moment.

First, model capability crossed a threshold. Frontier models became reliable enough at reasoning, tool use, and following multi-step instructions that a well-engineered agent can carry a real task to completion in many domains, not just draft a suggestion for a human to finish. Second, the surrounding engineering matured. Retrieval, orchestration frameworks, tool-calling standards, and evaluation tooling made it feasible to build agents that operate inside enterprise systems with acceptable reliability. Third, the economic incentive became overwhelming. When one agent can do the work of many licensed users, a vendor that keeps charging per seat is effectively pricing itself out of the value it creates, and a competitor that prices on outcomes can capture it.

The market data tracks this. Industry analyses in 2025 and 2026 generally show seat-based pricing in retreat and usage- and outcome-based models rising, with hybrid approaches becoming the default among incumbents adding AI. Deloitte's technology predictions and Bain's technology research both describe incumbents layering consumption and outcome metrics onto subscriptions rather than ripping out the old model overnight. The direction is consistent even where exact figures differ between sources: the unit of value is moving from the seat toward the task. For a broader view of how agents are absorbing entire workflows, see how AI agents are quietly replacing traditional software workflows.

Pricing is evolving along a spectrum from per-seat subscriptions, through consumption-based metering, to outcome and value-based models, with most vendors running hybrids during the transition. Each step changes what the buyer is paying for and who carries the risk if the work is not done.

| Pricing model | What the buyer pays for | Who bears delivery risk | Best fit | Key weakness |

|---|---|---|---|---|

| Per-seat subscription | Access per named user | Buyer (they must use it) | Tools humans operate daily | Breaks when agents replace seats |

| Consumption / usage | Volume of actions, tokens, or runs | Shared | Variable, bursty workloads | Unpredictable bills; misaligned with value |

| Per-outcome | Each completed unit of work | Vendor (no result, reduced or no charge) | Discrete, verifiable outcomes | Hard to define and attribute outcomes |

| Value / outcome share | A share of measured savings or revenue | Vendor (paid on results) | High-value, measurable business impact | Attribution disputes; complex contracts |

| Hybrid (platform + outcomes) | A base fee plus outcome or usage charges | Shared | Most enterprise transitions | Complexity; harder to forecast |

Real examples illustrate the endpoints. Intercom priced its Fin support agent at a flat fee per successful resolution, where an outcome is a resolved conversation or a configured handoff, and the customer is not charged when the agent fails to resolve. The company has documented this approach publicly, including how it defines and meters an outcome and how it builds performance guarantees into contracts (Intercom on building outcome-based pricing). Salesforce, by contrast, has cycled through several structures for Agentforce, from a per-conversation charge to a flexible credit-based consumption model, then layered on per-user options, illustrating how hard it is to settle on one metric (Salesforce flexible Agentforce pricing). The lesson is not that one model wins. It is that outcome alignment is the destination and hybrids are the road.

Outcome pricing sounds clean and is operationally messy. Three questions decide whether it works:

Vendors that answer these crisply can charge confidently on outcomes. Those that cannot retreat to consumption or hybrid models, which is why the middle of the spectrum is so crowded today.

Agent-as-a-service compresses gross margins because serving the product now carries a real, variable cost of goods sold: model inference, evaluation, and human oversight. This is the single most important and least appreciated consequence of the shift, and it inverts a core assumption of the SaaS playbook.

Classic SaaS enjoyed near-zero marginal cost. Once the software was built, serving one more customer cost almost nothing, which is why gross margins commonly sat in the 70 to 80 percent range and why the model attracted so much capital. AaaS does not have that luxury. Every completed outcome may require multiple model calls, retrieval over large context, retries, and verification. Industry analyses through 2026 generally describe AI-native gross margins running well below the SaaS norm, with inference standing out as a structural levy that scales with usage rather than disappearing at scale. Whether a given source pegs the gap at twenty or thirty points, the qualitative point holds: inference is COGS, and COGS scales with the work delivered.

Two further costs are easy to overlook in financial models:

The good news is that AaaS unit economics are highly sensitive to design choices, many made years before the cost appears on a P&L. The levers that matter most:

The strategic implication is stark: in AaaS, engineering discipline around inference cost is not an optimization detail. It is the difference between a fundable business and one that loses money on every outcome it sells. This is one of the strongest reasons to bring serious engineering depth to agent products. As an AI engineering and AI agent development partner, Mind Supernova works with enterprise teams precisely on this layer, designing model routing, evaluation harnesses, and cost-controlled architectures so that outcome-priced products are defensible on margin and not just impressive in a demo.

In an agent-as-a-service world, moats shift from owning features to owning the assets and reliability that competitors cannot quickly copy, because the underlying models are largely shared and rentable. If everyone can call the same frontier model, the model itself is not a moat. Defensibility has to come from somewhere else.

Four durable sources of advantage stand out:

Notably, the same economics that pressure margins also create a moat that pure SaaS never had. Software that reliably converts compute into outcomes at a controlled cost, priced to scale with value, is genuinely hard to replicate, because a competitor faces the identical inference economics and must solve the same reliability problem to compete. The margin gap is, in part, the price of the moat. For CTOs weighing where to place these bets across build, buy, and partner, our CTO guide to agentic AI strategic investments goes deeper on the investment framing, and the broader architecture is covered in the enterprise AI stack for 2026.

For buyers, agent-as-a-service offers tighter alignment between spend and value but introduces new risks around outcome attribution, accountability, and a deeper form of lock-in. The procurement conversation changes in concrete ways.

On the upside, outcome pricing aligns cost with realized value. Instead of paying for shelfware, the buyer pays when work is done. Budgeting can shift from a fixed software line to a variable cost tied to throughput, which is attractive when value is clear and measurable. Done well, this also forces vendors to share delivery risk, which is a healthier dynamic than paying full price regardless of usage.

The risks, however, are real and need active management:

For builders, the shift means re-architecting both the product and the business model around outcomes, while protecting gross margin through engineering discipline and choosing where on the spectrum to compete. This is a harder transition than adding an AI feature, because it touches pricing, finance, product, and go-to-market simultaneously.

The strategic decisions that matter most:

Many teams underestimate the engineering required to make outcome-priced agents reliable and economical enough to stand behind contractually. Designing the routing, evaluation, guardrails, and integration depth that turn a demo into a defensible product is specialized work. This is where an experienced AI agent development partner such as Mind Supernova can compress the learning curve, helping enterprise and SaaS teams build agents that are accountable, cost-controlled, and ready for outcome-based commercial models.

The pattern is already visible across several categories, even though the term itself is still settling. In customer support, agents that charge per resolution rather than per seat are the clearest production example of the model. In sales development, agents that qualify leads or book meetings and are priced per qualified outcome are emerging. In software engineering, coding agents that complete tasks and pull requests point toward outcome framing, even where pricing is still consumption-based. In finance and operations, agents that reconcile transactions, process invoices, or handle routine compliance reviews are being positioned as digital workers measured by cases cleared rather than licenses sold.

What these examples share is a reframing of the vendor relationship from supplier of tools to provider of work, sometimes described as buying "digital labor." That framing is marketing-friendly, but the underlying reality is exactly the business-model shift this article describes: the unit of value has moved from access to outcome. The categories where AaaS lands first are those with high-volume, verifiable, bounded tasks, because those are the outcomes that are easy to define, easy to attribute, and economical to deliver reliably.

The main risks of AaaS are margin fragility, reliability and trust failures, attribution and pricing disputes, and regulatory or accountability exposure when agents act autonomously. Each can sink an otherwise promising product.

The shift from SaaS to agent-as-a-service rewards deliberate, staged moves over either complacency or a reckless full rewrite. The recommendations differ for vendors and buyers, but both come down to discipline around outcomes, economics, and trust.

Agent-as-a-service is a software business model where a vendor sells completed work performed by autonomous AI agents and charges for the outcome, such as a resolved ticket or processed invoice, rather than charging for per-seat access to a tool a human operates. The software fades into the background and the result becomes the product.

SaaS sells a capability and charges for access, usually per seat, while the human does the work. AaaS sells the work itself and charges for the result, because the agent completes the task with limited human involvement. The unit of value shifts from a seat or feature to a completed outcome.

Industry analyses through 2025 and 2026 generally show seat-based pricing losing share to usage- and outcome-based models, with hybrid approaches becoming the default among incumbents adding AI. The exact figures vary by source, but the direction is consistent: pricing is moving from access toward consumption and outcomes.

Because serving an agent product carries a real, variable cost of goods sold. Every completed outcome can require multiple model calls, retrieval, retries, evaluation, and human oversight. That inference and oversight cost scales with usage, compressing the near-zero marginal cost and 70 to 80 percent gross margins that classic SaaS enjoyed.

Outcome-based pricing charges the customer for each completed unit of work, or a share of measured value, rather than for access or raw usage. A common example is charging per successfully resolved support conversation, with reduced or no charge when the agent fails. It aligns cost with value but requires precise, auditable outcome definitions.

The biggest buyer risks are disputes over how outcomes are defined and metered, unclear accountability when agents act autonomously, a deeper form of lock-in as agents embed in workflows and accumulate context, and volatile bills under variable pricing. Buyers should secure auditable metering, clear liability terms, data portability, and spend caps before committing.

No. Some markets reward a strong copilot that keeps humans in control, and not every workflow has verifiable, bounded outcomes suited to outcome pricing. The right move is to choose a position on the tool-to-agent spectrum deliberately, based on outcome verifiability, risk tolerance, and the level of trust buyers place in autonomous action in your domain.

The move from SaaS to agent-as-a-service is a business-model shift, not a feature trend. When software stops enabling work and starts doing it, the logic of selling seats collapses, and value migrates toward completed outcomes. That single change ripples through pricing, where hybrids bridge the path to outcome alignment; through unit economics, where inference and oversight become real cost of goods sold; through moats, which now rest on data, reliability, integration depth, and trust; and through the relationship between buyers and vendors, which becomes a negotiation over outcomes, accountability, and lock-in.

The winners on both sides will be the ones who treat this with engineering and commercial discipline rather than hype. For vendors, that means protecting margin by design, proving outcomes, and pricing to share risk. For buyers, it means piloting on measurable work, demanding auditable terms, and guarding against the deeper lock-in that comes with handing work to an agent. The teams that build agents which are reliable, cost-controlled, and genuinely accountable are the ones who will earn the right to charge for outcomes. If you are weighing how to architect, price, or build for this shift, the practical next step is to model the unit economics of a single bounded workflow end to end, and to bring serious AI engineering depth to the parts that decide whether outcome pricing is defensible or ruinous.

Custom ERP vs off-the-shelf SAP and Oracle: when packaged ERP fails, the composable alternative, and a clear b...

How to build a compliant digital wallet in 2026: architecture, double-entry ledgers, PCI DSS, PSD2, KYC/AML, s...

Monolith, microservices, or modular monolith in 2026? A decision framework, trade-offs, and real cases to choo...